In this week's edition of The Pointillist, a focus on the carrots and sticks of climate mitigation policy – with a special focus on emerging science of policy mixes and policy interactions. Insights into the dismantling of New Zealand's policy response to climate change, the global resurgence of industrial policy, the complementarity of emissions pricing, and China's looming disruption of food export markets.

We are lucky to not live in a culture of shameless climate denial. Most New Zealand politicians know that they must at least acknowledge the bare facts of climate change to appear credible to voters.

And yet this hasn’t prevented a major dismantling of New Zealand’s climate mitigation policy. A variety of regulations, standards and government budget lines have been suspended. Local councils have been admonished for efforts to reduce emissions. Recently, legislation was announced to prevent the courts from findings of liability for tort for losses and damages caused by greenhouse gas emissions.

Rhetorically, New Zealand might be a long way from Trump’s America, where climate change is glibly dismissed as a ‘hoax’ and a ‘con job’. Practically, however, the walkbacks on domestic policy are not so far apart.

To square this circle, the defenders of New Zealand’s policy backtrack argue that climate mitigation should be managed by Parliament at the national level, and that our national response is satisfied by the New Zealand Emissions Trading Scheme (NZ ETS) and the Climate Change Response Act 2022.

This would be well and good if this centralized policy framework was driving sufficient emissions reductions – but it is not. As Treasury concluded in its Budget Economic and Fiscal Update 2026: ‘Sizeable offshore abatement would be needed to meet NDC1 on top of domestic commitments without other interventions’. Meanwhile, the Coalition Government is opposed to spending on offshore abatement; it has not restored market confidence nor a meaningful price signal to the NZ ETS; and it isn’t disposed to other domestic interventions (although the Hormuz crisis has triggered a smattering of transition-oriented announcements).

I have previously written about New Zealand’s climate mitigation policy for Policy Quarterly, initially on the insufficiency of emissions pricing alone and the need for comprehensive policy mixes for effective mitigation.

The first of those articles prompted a longform critique from Matt Burgess, his last report for the New Zealand Initiative (titled Pretence of Necessity) before he entered the National Party in 2022 and eventually became the Prime Minister’s chief policy advisor (2024–2025).

As I noted then, his report is unreliable: scantily referenced, dependent on self-citations from his own blog, and flagrantly misleading in its interpretations of the science of net-zero. So I was not surprised to see Burgess in the news as the staffer who received the briefing note from Z Energy and Fonterra on excluding climate-related damages from common law actions (or torts), arranged by private email and delivered in hard copy to avoid the Official Information Act 1982. Such an unserious approach to climate change mitigation cannot survive scrutiny, so it resorts to other means, such as circumventing the rules of public transparency, to project its political influence.

Yet this approach is winning for now. New Zealand’s climate strategy today is essentially this: if we hold faith in an idealized version of the NZ ETS that exists in theory only, and we neglect the problems and constraints of the NZ ETS we actually have, then we can pretend to be committed to our climate targets while simultaneously decommissioning and obstructing the initiatives that might actually get us there.

This edition of The Pointillist brings together recent evidence – for whatever it's worth these days – to show that this strategy is destined for failure. If we want an effective response to the Paris Agreement targets, and also to capture the economic upsides of transitions to net-zero and nature-positive, we need a strategic policy mix that drives the change we want to see.

One of the high-level narrative shifts that occurred recently is the World Bank’s endorsement of industrial policy.

The publication of the April 2026 report, Industrial Policy for Development, spawned a flurry of overblown headlines, like this from WSJ:

World Bank Embraces Industrial Policy, Abandoning Three Decades of Stigma.

Actually, it's more a vibe shift than a u-turn. As chief economist, Indermit Gill, put it in The Economist, the World Bank is only shifting its emphasis on an ancient policy question: ‘Should a government ever load the dice in favour of a “strategic” activity?’

Thirty years ago, the World Bank gave ‘a weakly qualified no’. Now, the World Bank is giving ‘a highly qualified yes’ which takes into consideration ‘a mountain of evidence amassed since then’.

Others draw far more muscular conclusions from this same ‘mountain of evidence’, not least of whom is Mariana Mazzucato, one of the more prominent advocates of industrial policy in recent years.

I return to the issue of industrial strategy below, but one immediate upshot is the World Bank’s recognition of the importance of policy mixes:

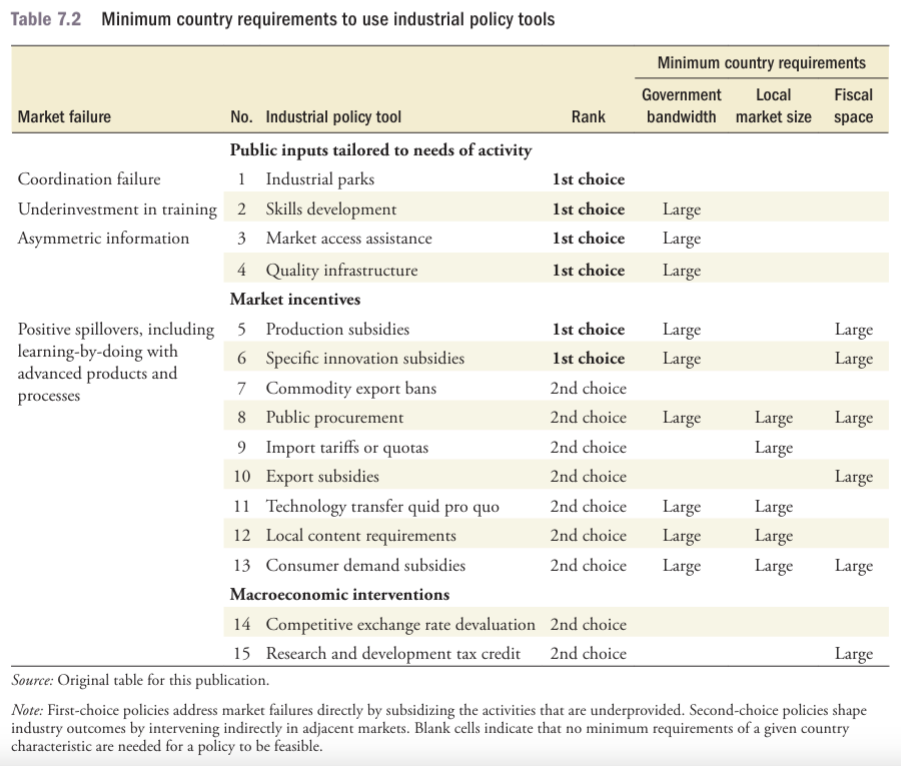

Once a government decides to expand a particular business activity, the central question becomes how best to promote it. Which industrial policy tools offer the greatest potential to stimulate growth, and how does this depend on country context and constraints?

The table below summarizes its view on defensible tools, as well as the minimum country requirements to successfully implement these.

There is now a growing empirical literature on the effectiveness of policy mixes for climate mitigation. This refers to a portfolio or ensemble of multiple policy instruments that are strategically selected to drive technological and behavioural change, and to neutralize the barriers to the effective implementation of policy.

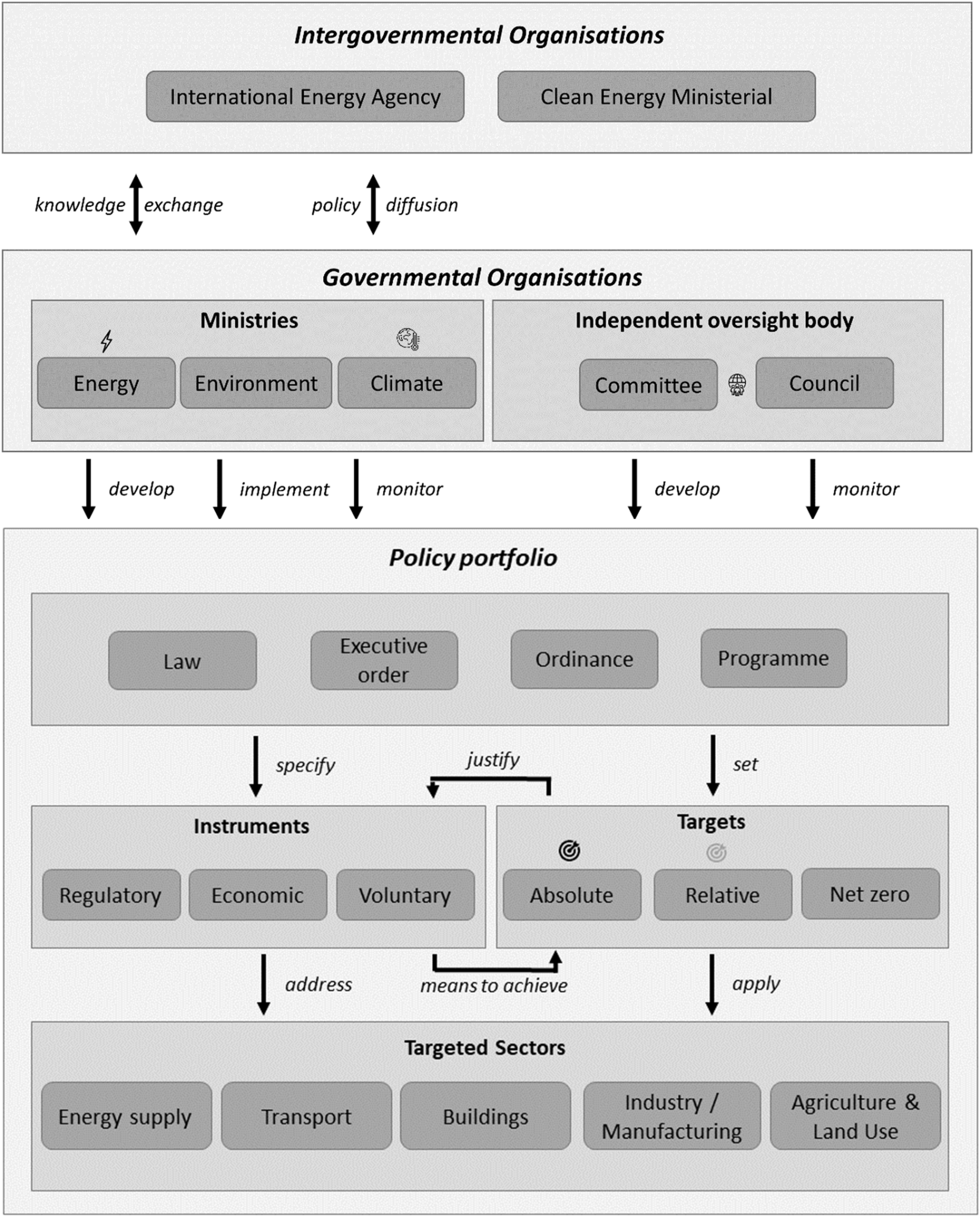

A new analysis of 43 countries by Theodoros Arvanitopoulos et al. (2026) finds that climate policy portfolios resulted in 27.5 GtCO2 of avoided emissions over the period 2000–2022, of which 14.6 GtCO2 were in the BRIICS countries. It attributes this effectiveness to the interactions between targets, policy instruments, governance institutions and transnational policy transfer (see the figure below). The authors conclude that:

... rather than single instrument dominance, policy mixes - including those comprising different instrument types – tend to be more effective for multiple reasons including: mutual reinforcement and positive spillovers; complementary time-varying effects; capacity for policymakers to address multiple problems simultaneously.

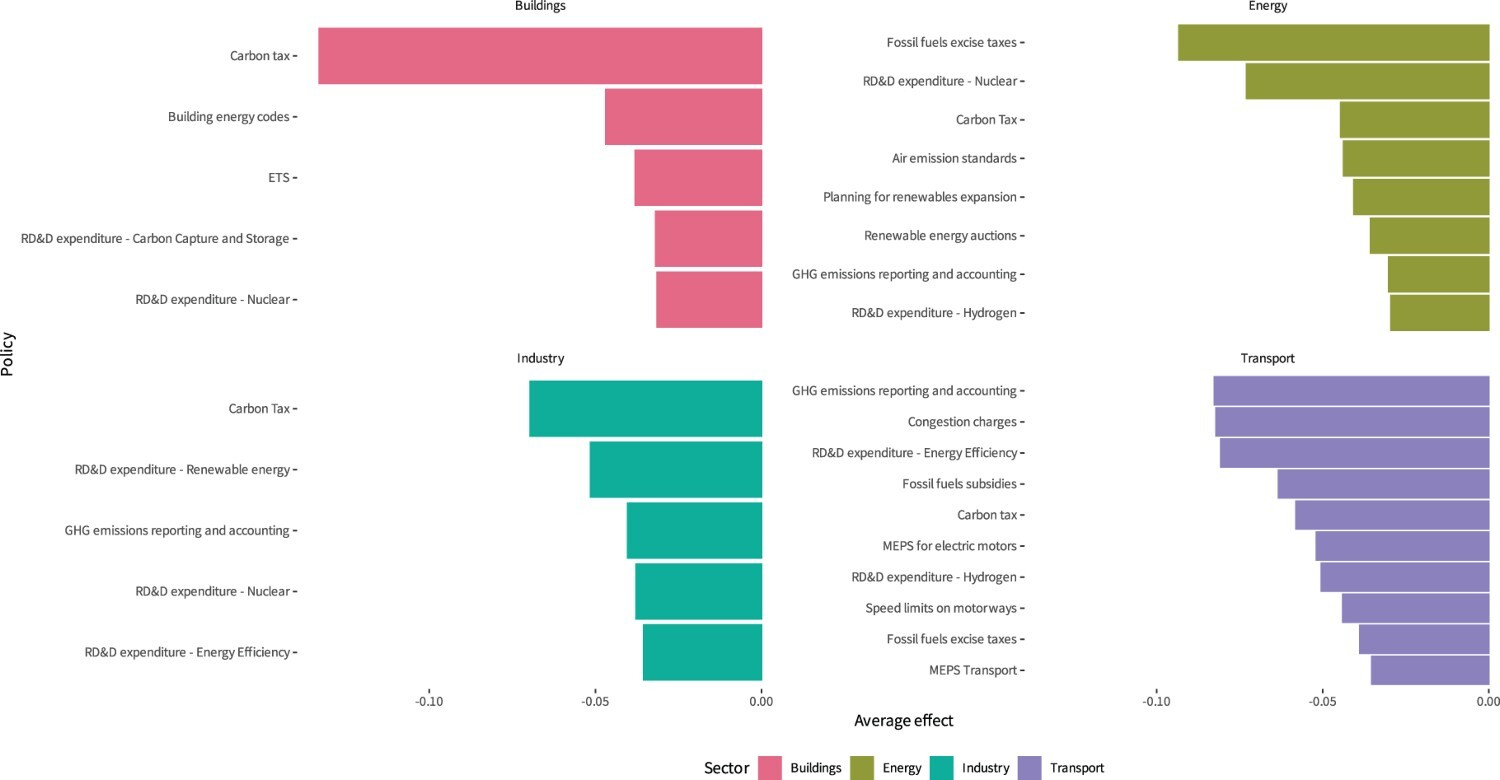

On the choice of instruments, a recent analysis by Xavier Fernández-i-Marín et al. (2026) used machine learning to assess 1,737 individual policies in 40 countries over 32 years (1990–2022) to identify which instruments are most effective and, therefore, ‘good for all seasons’ (see the chart below):

Importantly, our goal is not to identify the most effective combinations of climate policies but to pinpoint the individual policies that enhance any policy mix and that hence work for ‘all seasons’. Using a sports analogy, we are not interested in identifying the best ‘team’ of policies but rather in finding the best ‘players’ that can reliably enhance any team they join… Notably, implementing carbon pricing and taxation, along with investing in renewable energy and research, stand out as particularly reliable strategies for attaining significant reductions in CO2 emissions.

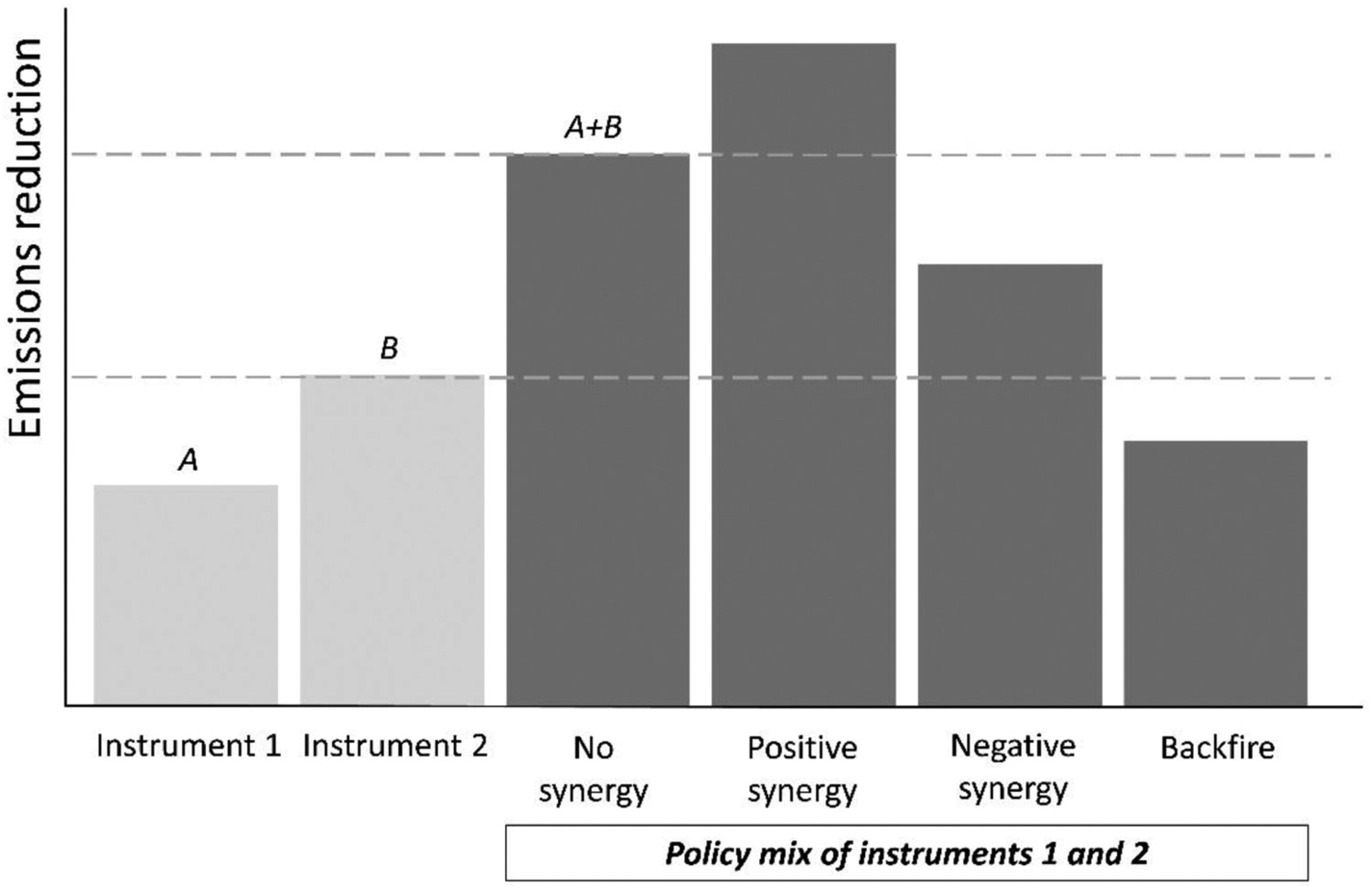

One of the worries about managing multiple policy instruments, especially in a policy context with a single dominant instrument like the NZ ETS, is that the policy interactions will necessarily be conflictual and self-defeating.

In theory, however, there are several possible types of interaction (as per the chart below). Yes, a policy backfire is possible, where the combined policy impact (A + B) is less than one or either of the instruments would have delivered on its own. There can also be a negative synergy where the combined policy impact of A and B is lower than the sum of the two policies individually. However, there can also be no synergy where the combined impact is simply the sum of A and B, or a positive synergy where the combined impact is greater than the sum of its parts, because the policies interact in catalytic and self-reinforcing ways.

Recent empirical research of policy mixes reinforces the potential for positive synergies. A touchstone paper by Annika Stechemesser et al. (2024) identified actual breaks or reductions in emissions in 41 countries over the past 25 years, then used machine learning to assess the underlying policy mixes. In assessing the underlying policy interactions, the paper draws the following conclusion:

we identified a number of policy instruments for which the empirical evidence suggests complementary effects. These include popular subsidy schemes and regulatory instruments such as bans, building codes, energy efficiency mandates, and labels, for which we found larger reduction effects in policy mixes as compared with the case of a stand-alone implementation. This suggests that some of these most widely used policy instruments are complementary or even reinforcing in policy mixes, which is in line with the theoretical understanding that these specific instruments alone often have a limited scope (for example, only new cars or new appliances) and are subject to rebound effects. Additional instruments such as pricing can effectively address both factors and thus generate positive synergy.

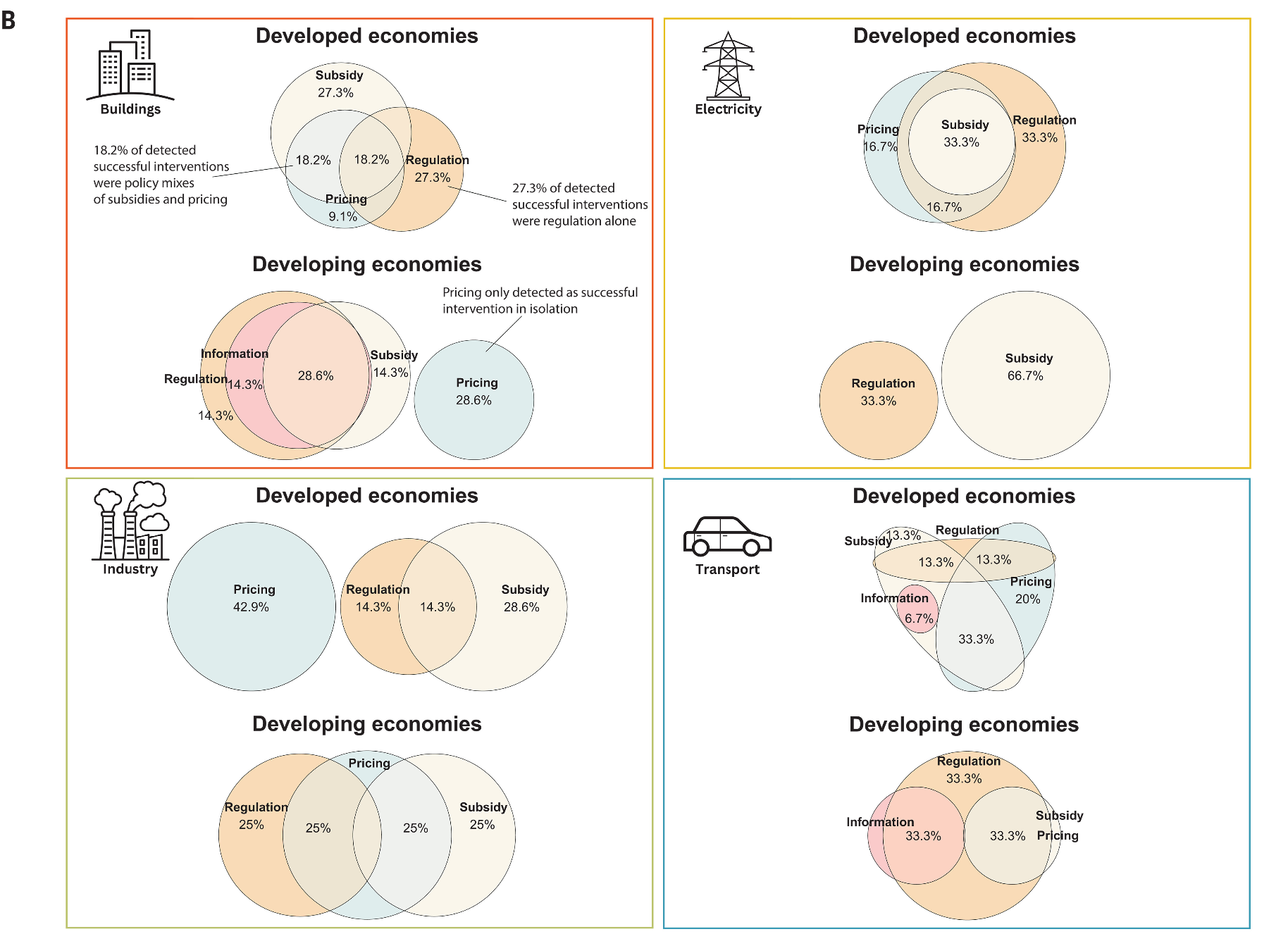

The chart below shows the overlapping policies that have driven emissions breaks in key sectors: buildings (red square), electricity (yellow), industry (green) and transport (blue). The effectiveness of overlapping policies varies across sectors, with the transport sector showing the highest potential for complementarities.

Transport-related subsidies are the most complementary instrument in developed economies, especially in combination with pricing, which accounts for 33% of all successful policy interventions. 20% of breaks in emissions involve pricing alone.

In the electricity sector, by contrast, regulation is the most effective stand-alone policy (33%). However, pricing emerges as a very important element of effective policy mixes, with 50% of all successful policy mixes including pricing.

None of this is to say that we shouldn’t worry about bad policy interactions. Of course, we should – and a thoughtless accumulation of overlapping policies is likely to create knots, incoherency, political backlashes, and ever diminishing returns.

However, not every policy interaction is bad and, moreover, we can manage negative synergies when we find them through better policy design.

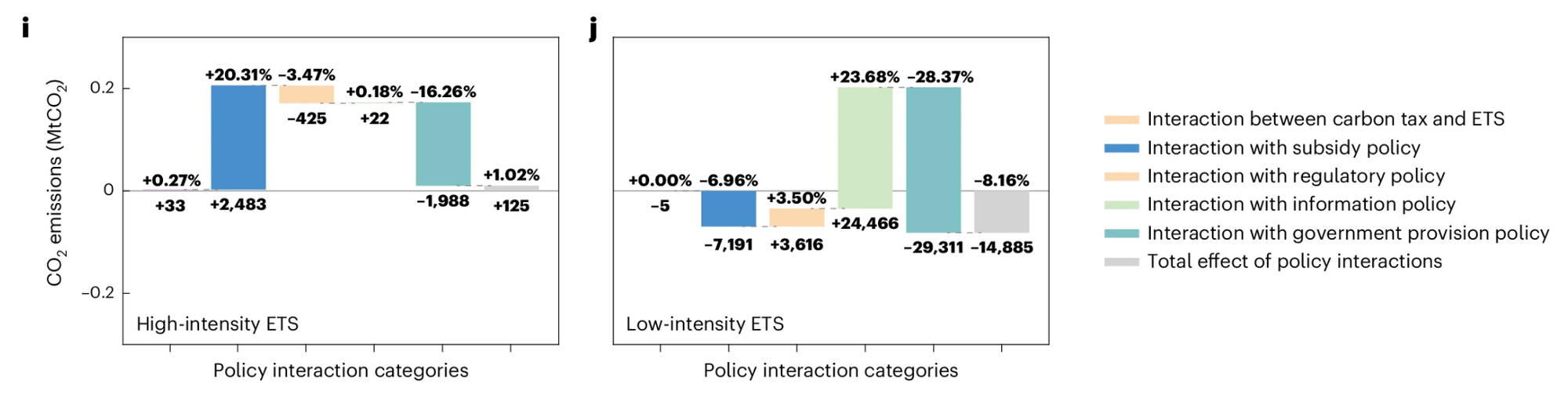

A new paper by Wu et al. (2026) undertakes a systematic global analysis of climate policy interactions, with a particular focus on countries (including New Zealand) that combine emissions pricing with other policy instruments. It identifies negative synergies in existing policy mixes and, by running counterfactual simulations, estimates that the effectiveness of emissions pricing could be improved by up to 22.3% by reducing policy conflicts.

Its comparison of high- and low-intensity ETS is also instructive (see the charts below). If the ETS is high-intensity, then the potential for distortions and conflicts from overlapping policies increases. However, when the ETS is low-intensity – with weak or volatile prices – the distortionary impacts are outweighed by the innovation benefits, resulting in policy interactions that drive additional emissions reductions.

Aligning subsidy and information policies with ETS maturity, while leveraging government provision instruments to ease adjustment costs, promotes more coherent mitigation outcomes… [I]n low-intensity ETSs, carbon pricing policies exhibit strong synergies with government provision policies. By supporting research and development and public infrastructure, such policies reduce compliance costs within the ETS cap and provide an early boost to decarbonization.

To be clear, the literature on policy mixes does not amount to a renunciation of emissions pricing. If anything, this literature reinforces the importance of emissions pricing being a part of the mix. But what it does reemphasise is the need for careful policy appraisal and design. As Wu et al. (2026) conclude:

A well-designed, interactive policy portfolio is crucial for effective climate change mitigation. Moreover, decarbonization rarely hinges on a single, comprehensive measure. Instead, it evolves incrementally, with earlier measures shaping the context in which subsequent policies operate.

On the matter of timing, there is also a growing literature on policy sequencing, which considers in which order that policies might be implemented to maximize the positive synergies and minimize the negative.

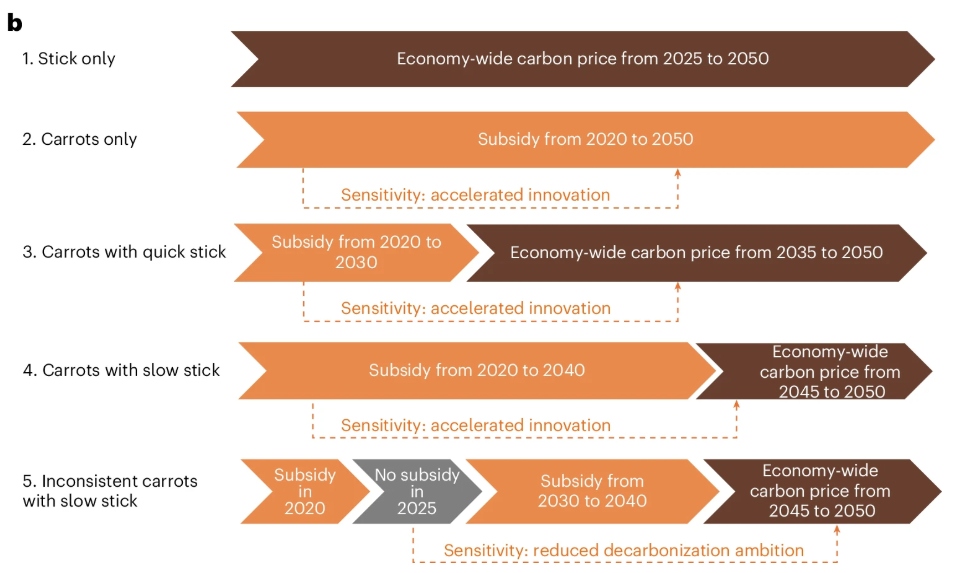

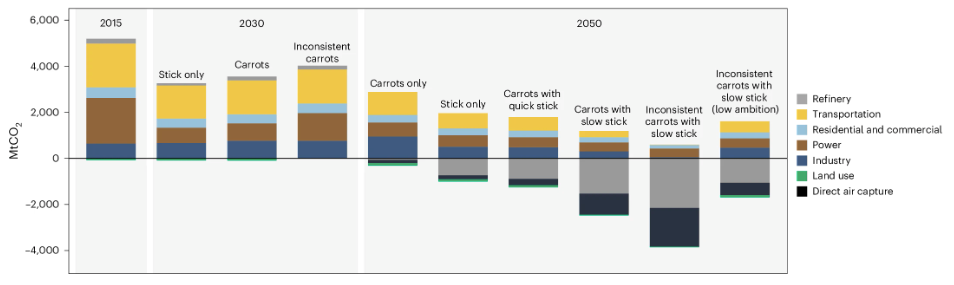

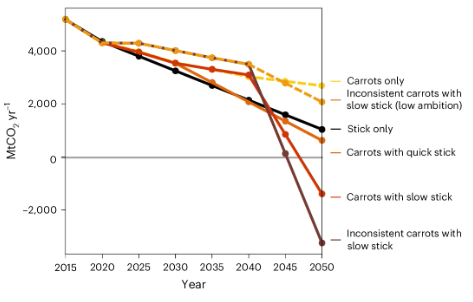

A recent paper by Huilin Luo et al. (2026) explores the intertemporal interactions between the sticks and carrots of policy. As the paper defines the problem:

A particular challenge is that sticks impose highly visible upfront costs on existing industries which are often well organized politically, along with voters who object to higher prices for energy and other goods. In contrast, the costs of industrial policy carrots are often highly diffused and abstract (for example, larger state budgets) while the benefits can be concentrated on favoured industries and other politically organized segments of society. Given this political reality, it may be expedient for climate policy strategies to begin with carrots and then transition to a greater role for sticks.

The paper creates a number of scenarios (see the figure below) where the ‘stick’ is emissions pricing and the ‘carrot’ is subsidies for green technology. The carrot-then-stick scenarios explore different combinations of pricing and subsidies over time.

What the scenarios find is that sticks and carrots do work. Implemented independently, both can drive significant emissions reductions by 2030 against a 2015 baseline.

Beyond that timeframe, however, the carrots-only approach delivers diminishing returns, in part because the declining costs of new technologies begin to flatten out. What works much better – and better even than a sticks-only approach – are the carrots-then-sticks scenarios:

Compared with ‘stick only’, carrots support the investments in supply-side technologies such as wind and solar power generation and accelerate the adoption of demand-side technologies such as EVs. Yet, compared with ‘stick only’, carrots that specifically support green technologies do not impose many negative impacts on fossil industry…

The paper's synopsis is this:

... we find that consistent carrots in the near term that are followed quickly by sticks can facilitate deep reductions in long-term emissions if this policy sequence accelerates innovation of clean technologies.

A recent OECD paper, Packaging and sequencing policies for more effective climate action, usefully sums up the policy relevance of this literature:

- Policies can interact negatively when targeting the same emissions base and market failure, but such negative impacts can be alleviated through careful policy design.

- Policymakers need to be aware of potential negative impacts and understand how to overcome them. Seemingly inconsequential design choices could significantly impact whether two policies work well in tandem.

- Sequencing of policies is critical, with some policies working well in sequence but not in parallel.

- Policies will interact differently in different sectors and across different jurisdictions.

- Policymakers need more evidence on what works and what doesn’t to make informed policy decisions.

Of course, card-carrying neoclassical economists might respond that they never denied that other policies might be effective; rather, they argued that such policies are inefficient, because non-pricing policies pre-empt the market’s capability to find least-cost abatement.

This relies, of course, on some rather heroic assumptions about the current state of markets – i.e. that markets have complete information, that markets are perfect except for the climate externality, and so on. But, more fatally, this view also neglects the costs of ineffectiveness. In other words, the focus on short-term cost-savings (or the imposition of high discount rates) obscures the costs of climate-related damages, as well as the foregone revenue from the innovation, productivity and growth that emerges through transitions.

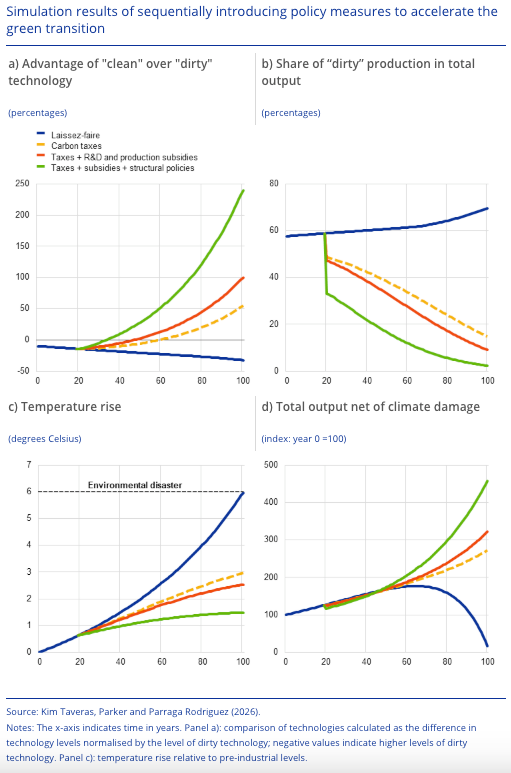

The European Central Bank (ECB) recently tried to do better with its economic modelling. Building on work by Daron Acemoglu et al. (2012) on directed technological change, the ECB built a model to simulate four scenarios, each with a different policy mix – from a laissez faire scenario with no new policy, to a first-best approach that relies on emissions pricing only, to more diverse policy mixes that correct misaligned private incentives and address structural barriers to the green transition.

As shown in Panel D, the effectiveness of policy mixes that actually reduce emissions are well-compensated for by the cost-savings from avoiding catastrophic climate change. The laissez faire approach (the blue line) falls off a cliff in terms of reduced economic output, while the more ambitious approaches to climate action pay dividends.

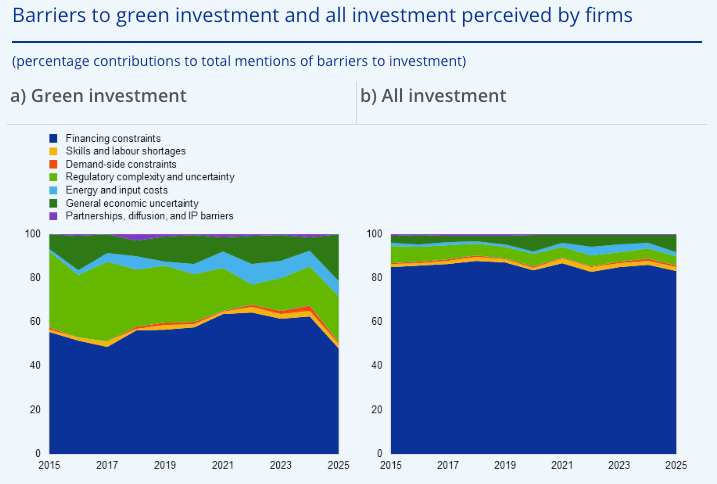

Incidentally, the paper also offers some firm-level insights on perceived barriers to green investment. Financing constraints are identified as a major constraint for all types of investment. However, the constraints for green investment are significantly more diverse, with regulatory complexity and uncertainty playing a major role, as well as a growing role for economic uncertainty.

The lesson the authors draw is this:

The combined existing barriers to the green transition are insurmountable without policy intervention.

If government wish for private finance to enable the transition, it is not a matter of standing back, but rather playing a proactive role in creating an enabling environment for investment which reduce regulatory complexity, reduces risk, and disinhibits financing.

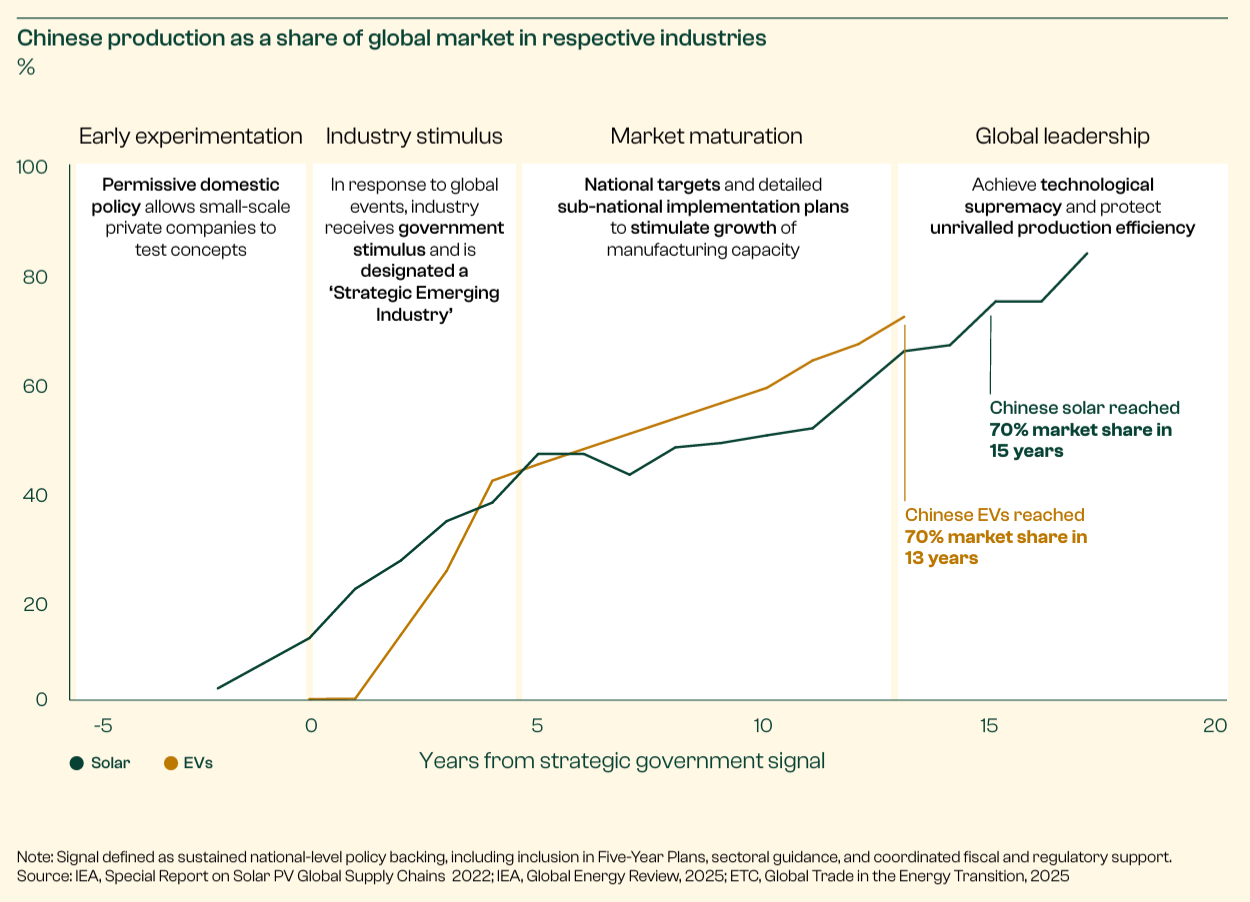

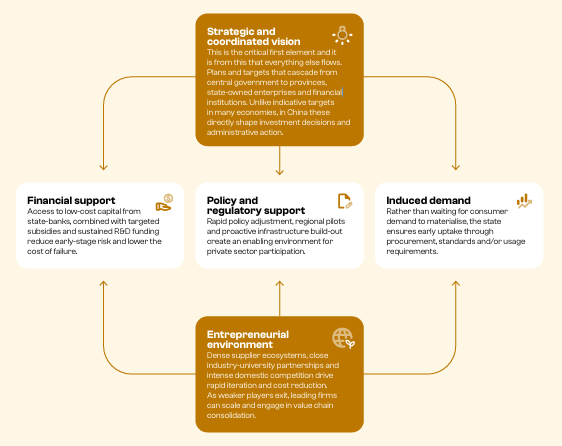

The potential of policy mixes to serve economic and geopolitical strategy is exemplified by the power of Chinese industrial policy, which has captured the global electro-tech supply chain. If this new SystemIQ report is anything to go by, this same approach is about to be directed toward the food system.

To recap, China’s rapid dominance in electrotech is an exemplar in modern industrial strategy. National direction is set by instruments like the Five-Year Plan, then outcomes emerge through experimentation at the provincial, municipal and firm levels (see below).

China is now adapting this approach for the food system, driven by national interests to secure food supply and reduce international dependencies. The recently released 15th Five-Year Plan (2026-2030) builds upon its predecessor by prioriziting food security, agricultural modernisation, and the diversification of food supply systems.

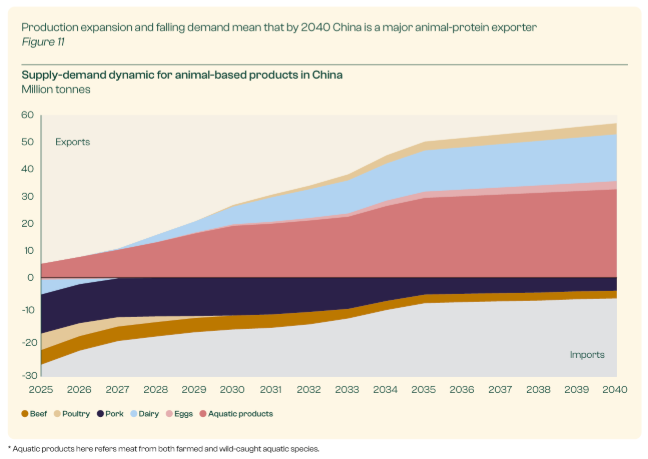

The projected effects of this approach for agricultural exporters like New Zealand are jaw-dropping (see figure below). If China meets its targets, it is projected to flip from a net importer of dairy to a next exporter over the next few years. Through the 2030s and 2040s, China is a major exporter of dairy. Only beef imports are marginally affected from the planned transition of China’s food system.

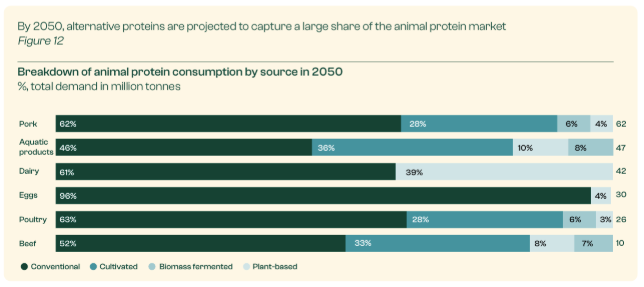

What is driving this is a combination of improved efficiencies and reduced food waste, onshoring of supply through cultivation, and the growth of alternative proteins from precision fermentation. It doesn’t tell a story of total substitution, rather a story of diversification (see chart below) which reduces offshore dependencies.

This has echoes of developments in processed wood markets, where China has begun exporting large volumes of laminated veneer lumber (LVL) at a low cost. It draws in unprocessed logs from diverse sources, including New Zealand radiata, then recycles it back to global markets as LVL with on-demand wood blends, quality grades and certification requirements. The landed price is highly competitive, potentially contributing to the malaise of wood processing in open markets like New Zealand.

The common denominator is a strategic policy mix to deliver large-scale transformative change that serves China's geopolitical interests (see the figure below). Plans and targets, like the commitments in the Five Year Plan, are transmitted through the economy to induce coordination and direction. A highly competitive entrepreneurial environment drives innovation and efficiencies on the supply-side. Then the carrots and sticks of fiscal and regulatory policy are used to derisk innovation and create entry points to market, to induce consumer demand for new products and technologies, and to steer markets toward the achievement of national strategic goals.

To finish, let us return to the theme of industrial policy.

This Nature perspective by Jonas Meckling (2025) is vital reading on ‘the geoeconomic turn in decarbonization’:

... the rise of industrial policy marks a geoeconomic turn in the politics of decarbonization: global competition for the economic benefits of decarbonization has emerged alongside global cooperation on the costs of mitigation. Macro forces suggest that this will probably be a sustained shift. Nationalism and great power rivalry are fuelling it.

The major story, as I’ve said before, is China’s rapid dominance in electrotech:

By 2023, China had accumulated more than two-thirds—and in many cases, above 90%—of global manufacturing capacity for major clean energy technologies, including solar photovoltaics, batteries, electric vehicles, electrolysers and heat pumps. In addition, in 2023, China provided the majority of refined lithium, cobalt, graphite and rare earths globally, as well as holding substantial stakes in the markets for refined copper and nickel.

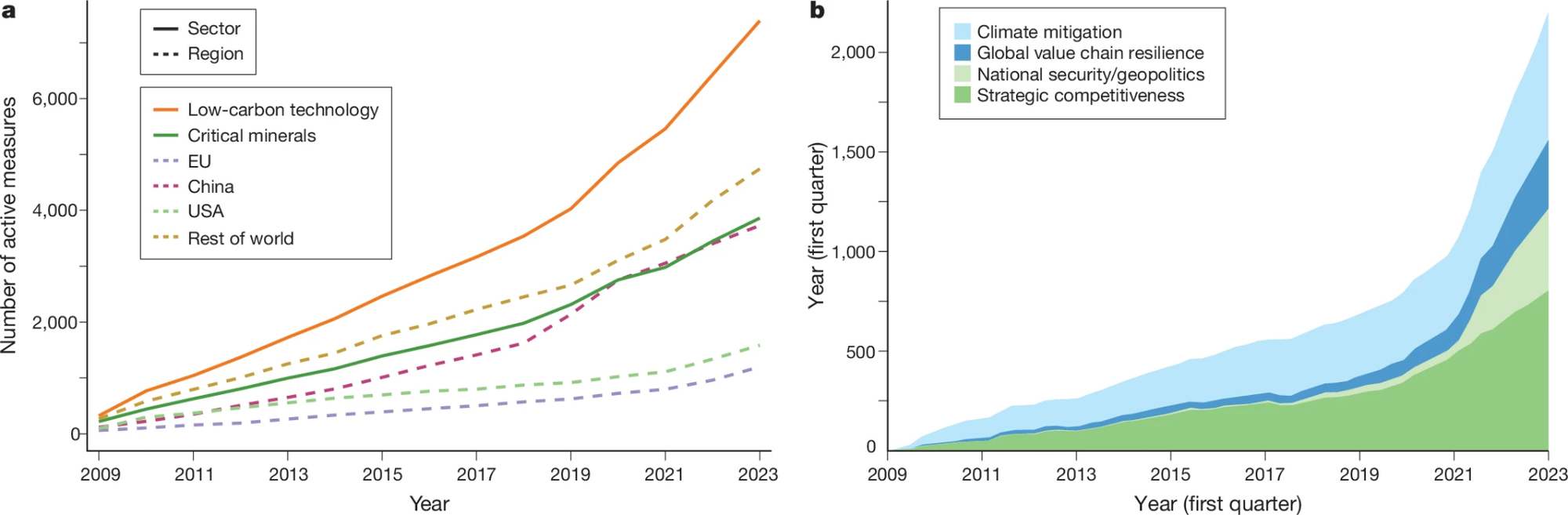

But this is a wider trend, not least because China’s rise induces policy responses from other economic powers like the US and EU. The chart below shows the slow-building accumulation of active industrial policy measures, which accelerated this decade. Panel A shows low-carbon technology and critical minerals by target sector and region. Panel B shows the motives that policymakers ascribe to policy. Notably, climate mitigation has stayed relatively steady in recent years, but the rationale for industrial policy has grown for value chain resilience, national security and strategic competitiveness.

This, of course, begs the question of New Zealand’s positioning in this new world. New Zealand is not China, indeed radically different in size, industrial capacity and political culture. It is far from obvious that New Zealand can take any direct lessons from the Chinese experience. Nevertheless, New Zealand has a history of innovation – even world-leading innovation – and these successes often emerged from a framework of directed innovation.

New Zealand’s space industry is a contemporary example. But a truly transformative example – for good and bad – is the New Zealand Government’s cultivation of the Pinus radiata industry – from corralling interests around one exotic tree species a century ago, to creating early forestry assets through land-use policy and state employment programmes, to funding R&D and knowledge extension over many decades to vastly improve forest productivity. That history embodies all the nation-building potential of industrial policy, as well as its risks and opportunity costs.

But it can be done. New Zealand should not use its 'small country' status to rule itself out from high-growth economic opportunities that align with net-zero, nature-positive transitions. Previous analysis has identified innovation potential in agritech and the wider bioeconomy, waste-to-value, and geothermal energy – all sectors where we have a comparative advantage.

Moreover, others are doing industrial policy regardless, China most dramatically, but other countries also. We should not be indifferent to this. We should not operate as if we are in the global market that we wish the world to manifest: free, open, rule-bound, economically optimized. We need to develop strategy for the global market we are actually in, playing to our advantages and enhancing onshore value.

Meckling notes that green industrial policy (GIP) does not necessarily entail a closed economy; it can serve an open, export-oriented economy too (see the table below). For a small economy like ours, these policies will not alter the geopolitical winds, but they can be used to trim the sails, to ensure our economy generates domestic value, even in an era of competition among geopolitical behemoths.

Thanks for reading this far! If you haven't already, please subscribe to receive future content like this, as well as essays and transition-related briefings.